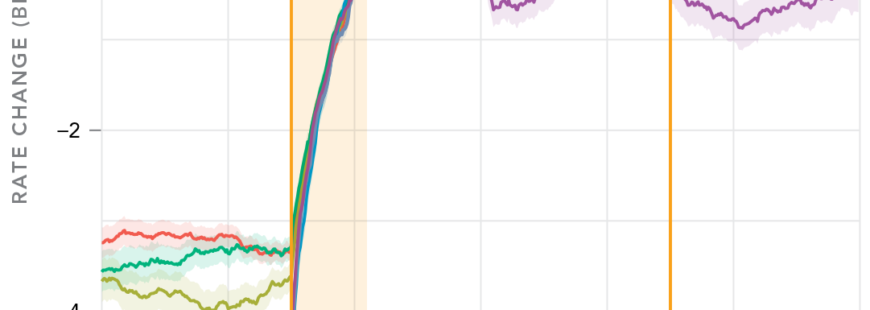

We’ve published a new trading research note “On the Limits of Markouts and Venue Curation” which highlights the challenges venues have in the use of markout to evaluate execution quality as they simply do not know the context or have enough information to truly measure the opportunity cost of not trading. We also demonstrate that markout is not just a characteristic of the venue or its order type logic, rather it is a characteristic of

READ MORE